Designing a 2028 Class 8 BEV That Actually Makes Money

What AI Gets Right, and What It Misses

Battery-electric trucks have been talked about for years. But the market reality in 2025 is more sobering than the headlines suggest. North American Class 8 BEV sales dropped roughly 80% in the first half of 2025 compared to the same period in 2024. That is not a blip — it is a signal that fleets are still not convinced the economics work.

Part of the reason sales dropped is simple: the economics of building BEV trucks have not worked for most OEMs outside China [16-19]. Battery costs, low production volumes, and warranty unknowns made the unit economics painful at best. Building a new category of vehicle is expensive, and most of that cost lands on the early units before scale kicks in.

The technology is genuinely improving though. Battery pack costs have fallen around 20% in the past two years alone. That matters because battery cost is the single biggest reason electric trucks are expensive to build and hard to price competitively. A 20% drop does not solve the problem overnight, but it changes what a well-designed 2028 truck could actually look like.

Yet most OEMs keep building anyway, even at a loss. Because sitting out the BEV market entirely means handing the customer relationship to Tesla and startups — possibly forever. It is less about confidence in the economics today and more about not losing the game by default.

One more assumption worth stating upfront. Chinese manufacturers have demonstrated that a truck can go from concept to market in roughly two years [14, 15]. Traditional US and European OEMs have historically taken four to five years [14, 15]. This blog assumes that gap gets closed — that the OEM in this scenario has fixed its internal product cycle and is operating at two-year speed. How they do that is a separate and genuinely hard problem. But if they cannot, the 2028 launch date slips to 2030 or 2032, and the competitive window narrows further.

That is the tension this piece tries to resolve: can an OEM actually design a Class 8 BEV in 2028 that makes money, without subsidies, and still win against the competition on fleet economics?.

What the Current Product Landscape Looks Like

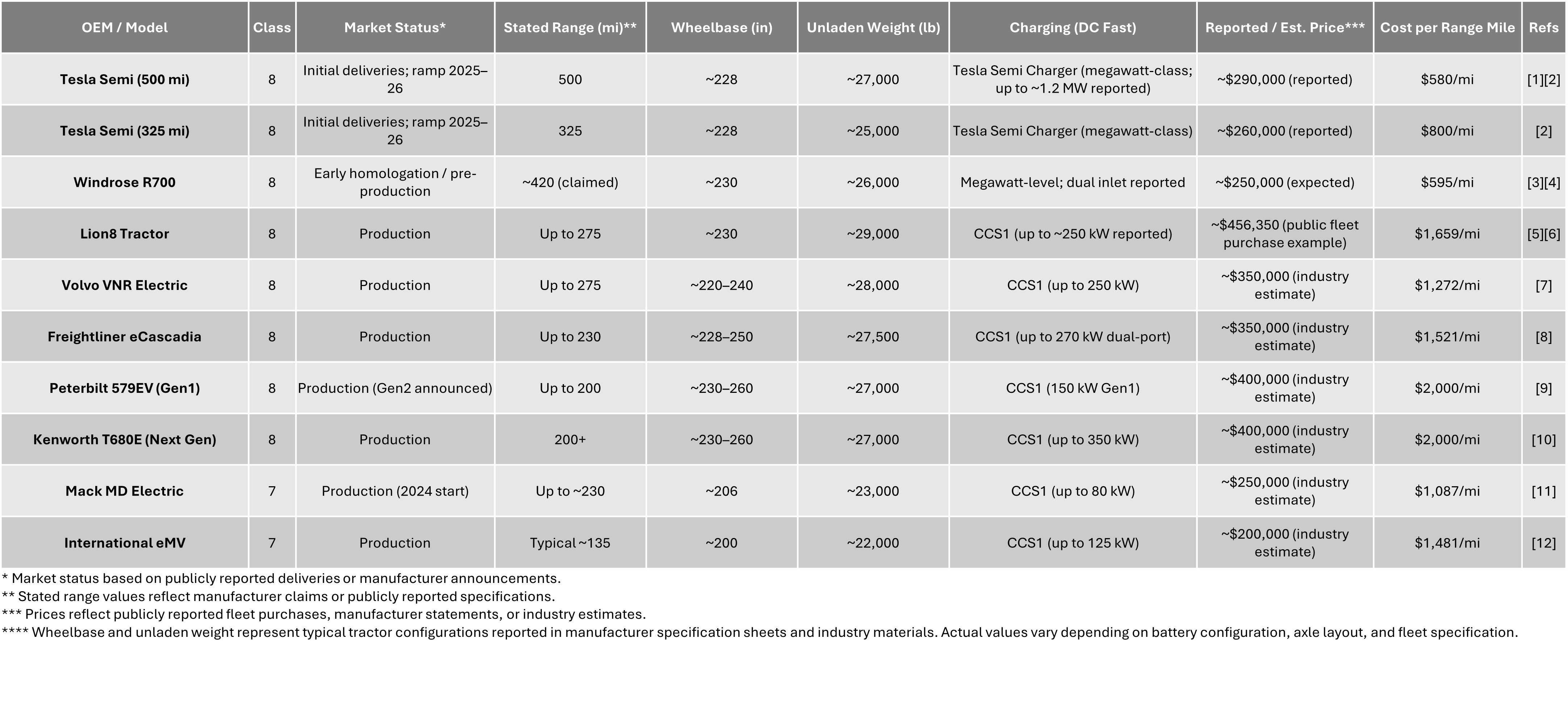

The current Class 7–8 BEV landscape is starting to take shape. Most trucks on the market today are designed for regional and short-haul use. Typical advertised ranges are around 200–300 miles, although a few newer platforms claim 400–500 miles. Most current trucks use CCS fast charging, while the next generation is starting to move toward megawatt-class charging (MCS).

To make this more concrete, the table below summarizes a sample of battery-electric truck platforms that are available today or publicly announced. I included range, charging, weight, estimated price, and a simple normalization: cost per mile of stated range.

Quick Takeaways From the Market Table

Even in a small sample, the variation is large:

Prices are all over the map (roughly $250k to $400k+ depending on platform and config).

Cost per “range mile” varies by ~3×, which highlights how expensive long range still is.

Most offerings look optimized for regional freight, not true coast-to-coast long-haul.

The data also hints at a key problem: more range usually means more battery, and battery is still the biggest cost and weight driver.

This sets up the strategic question that matters for OEM product planning.

The Real Question: What Would Be Competitive in 2028?

Truck programs take years to develop. A product launching in 2028 must be designed for where the market will be—not where it is today. That means making assumptions about:

Battery pack cost (especially the ex-China cost gap)

Charging infrastructure buildout (CCS vs MCS availability)

Fleet duty cycles and operational constraints

TCO expectations (and how strict fleets will be)

So I tested a simple idea:

If an OEM were designing a Class 8 BEV today for a 2028 launch, what specs would actually be competitive?

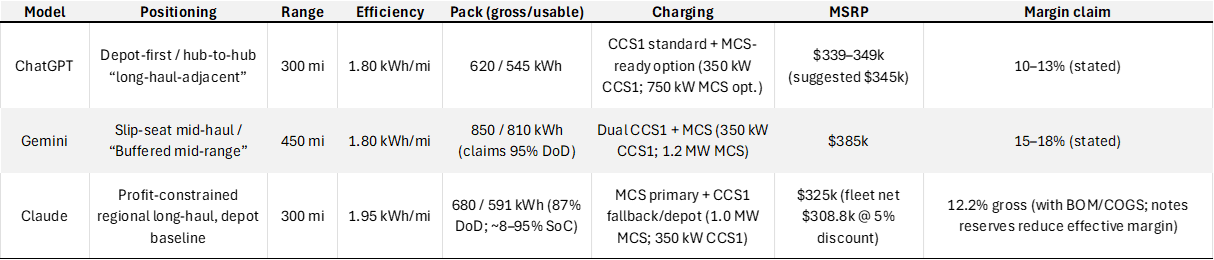

A Simple Experiment: Ask Multiple AI Systems the Same Prompt

To explore this, I asked three AI systems to act like the head of battery-electric truck development at a North American OEM. Each system received the same background briefing and the same constraints. The constraints were intentionally practical: ex-China pack cost ~$180–200/kWh, CCS1 common / MCS limited, ~$0.15/kWh electricity, and a requirement that fleet TCO beats diesel within 5 years (no subsidy dependence).

The goal was simple: propose a profit-constrained 2028 Class 8 BEV that can win on 5-year TCO without depending on regulation to force adoption.

Instead of pasting the full AI responses (they are long), I extracted the key specs into a clean comparison table below. If you want to see the exact prompt and the full unedited outputs from the three AI systems, I’ve posted them here.

What the AI Outputs Reveal

The table shows that the biggest disagreement is not about motors or software. It’s about one decision:

Do you carry more energy on the truck (bigger pack), or do you tighten the operating model (planned charging + predictable lanes)?

One approach goes for a bigger pack + longer range, which improves flexibility but pushes price, mass, and charging demands higher.

Another approach stays near ~300 miles, which makes the economics cleaner and the product easier to sell—but it requires route discipline (depot-first, hub-to-hub, one planned fast-charge stop if needed).

Charging strategy also splits: some outputs treat MCS as central, while others treat it as optional / future-ready.

Model-specific highlights:

As per ChatGPT, the winning move is to right-size the battery—avoid diesel-like range, target ~300 miles, and make the business case work with depot-first, predictable lanes.

As per Gemini, the truck should be designed for slip-seat mid-haul with a mid-day “splash” fast charge, so high utilization (not maximum range) drives TCO.

As per Claude, payload penalty changes which freight segments are viable (cube-limited vs weight-limited), and “profitability” should be viewed as gross margin minus warranty reserve and low-volume launch overhead.

In practice, early BEV tractors fit cube-limited freight (e.g., snack foods or packaged retail goods) better than weight-limited freight (e.g., bottled beverages or dense materials), because battery mass reduces payload headroom.

A Merged “Best-Fit” 2028 Spec

After comparing the three outputs, my conclusion is simple: the best answer is a merged spec that keeps the assumptions defensible and the product sellable.

My baseline positioning is:

Regional long-haul, depot-first, hub-to-hub lanes with one planned fast-charge stop where it matters.

My Take

The point of this exercise is not to claim AI can design a truck program. It is simpler: even when three models see the same facts, they make different tradeoffs. That clarifies the real design tension for 2028:

Range is expensive.

Battery cost and weight still dominate.

Charging reality shapes the product more than spec-sheet ambition.

A credible 2028 design must win on TCO and operational fit, not hype.

Tesla Semi at $260,000 resets the price benchmark and is hard to ignore. But price is not the only variable a fleet procurement team weighs.

A traditional OEM brings a nationwide dealer and service network that Tesla simply does not have today. For a fleet operator running 50 trucks, a broken truck sitting idle for three days waiting for a Tesla-certified technician is a real cost that does not show up on a spec sheet. Uptime is money, and fleets know this.

There is also a portfolio argument. Most fleets do not operate one truck type. They run day cabs, vocational trucks, refuse vehicles, and flatbeds alongside long-haul tractors. A traditional OEM can offer BEV solutions across that entire portfolio. Tesla cannot. That breadth matters during procurement conversations, especially at the enterprise level.

Finally, most large fleets will run mixed ICE and BEV for the next decade — the transition will not happen overnight. A fleet buying 200 diesel trucks and 30 BEV tractors from the same OEM has real negotiating leverage for bundled pricing, shared service contracts, and financing terms. That relationship advantage is invisible in a side-by-side spec comparison but very visible in the final purchase order.

Tesla wins on pure specs today. Traditional OEMs win on ecosystem, service depth, and fleet relationships — if they execute.

Reference List

[1] Tesla Semi product presentation / specs (official page)

[2] Tesla Semi reported pricing (standard ~325 mi ≈ $260k; long-range 500 mi ≈ $300k)

[2a] Tesla Semi 500-mile pricing reported at ~$290k (industry reporting), Yahoo Finance, Automotive World

[3] Windrose R700 product/pricing reporting (range ~420; price ~250k expected; MW charging, Chargedevs

[5] Lion Electric Lion8 tractor specs (OEM)

[6] Lion8 pricing evidence (public procurement/options sheet showing ~$456,350 base)

[7] Volvo VNR Electric specs (OEM; range up to 275; charging details)

[8] Freightliner eCascadia specs (OEM)

[9] Peterbilt 579EV specs (OEM)

[10] Kenworth T680E specs (OEM)

[11] Mack MD Electric specs (OEM; CCS1, DC 80 kW)

[12] International eMV specs (OEM)

[13] BloombergNEF (2025) Zero-Emission Commercial Vehicles Factbook (PDF)

[14] California ARB: Zero-Emission Class 8 Tractor Pricing Comparisons (avg price + context)

[14] Automotive product development: Accelerating to new horizons

[16] Bloomberg — Quebec Government Won't Rescue Bankrupt Lion Electric (May 2025)

[17] Reuters (Nikola losing hundreds of thousands per vehicle sold)

[18] Lion Electric Q3 2024 results (gross loss / negative gross profit)

[19] Industry context on cost gap + infrastructure