Do We Have Enough Minerals for the Energy Transition?

A stock vs flow reality check

I recently watched a TED-style talk by Matt Tilleard where he makes a compelling point: the current shift is less an energy transition and more a technology transition.

One idea that stood out was his claim that Earth has enough minerals to support a large-scale move to renewables and battery-electric systems. From a geological perspective, this is largely correct. The planet is not “running out” of lithium, copper, or rare earth elements.

But that raised a follow-up question for me:

Even if the minerals exist, can extraction, processing, and manufacturing capacity scale fast enough to meet near- and medium-term deployment goals?

This post is not a critique of Matt’s argument. It builds on it by adding a supply-chain and timing lens.

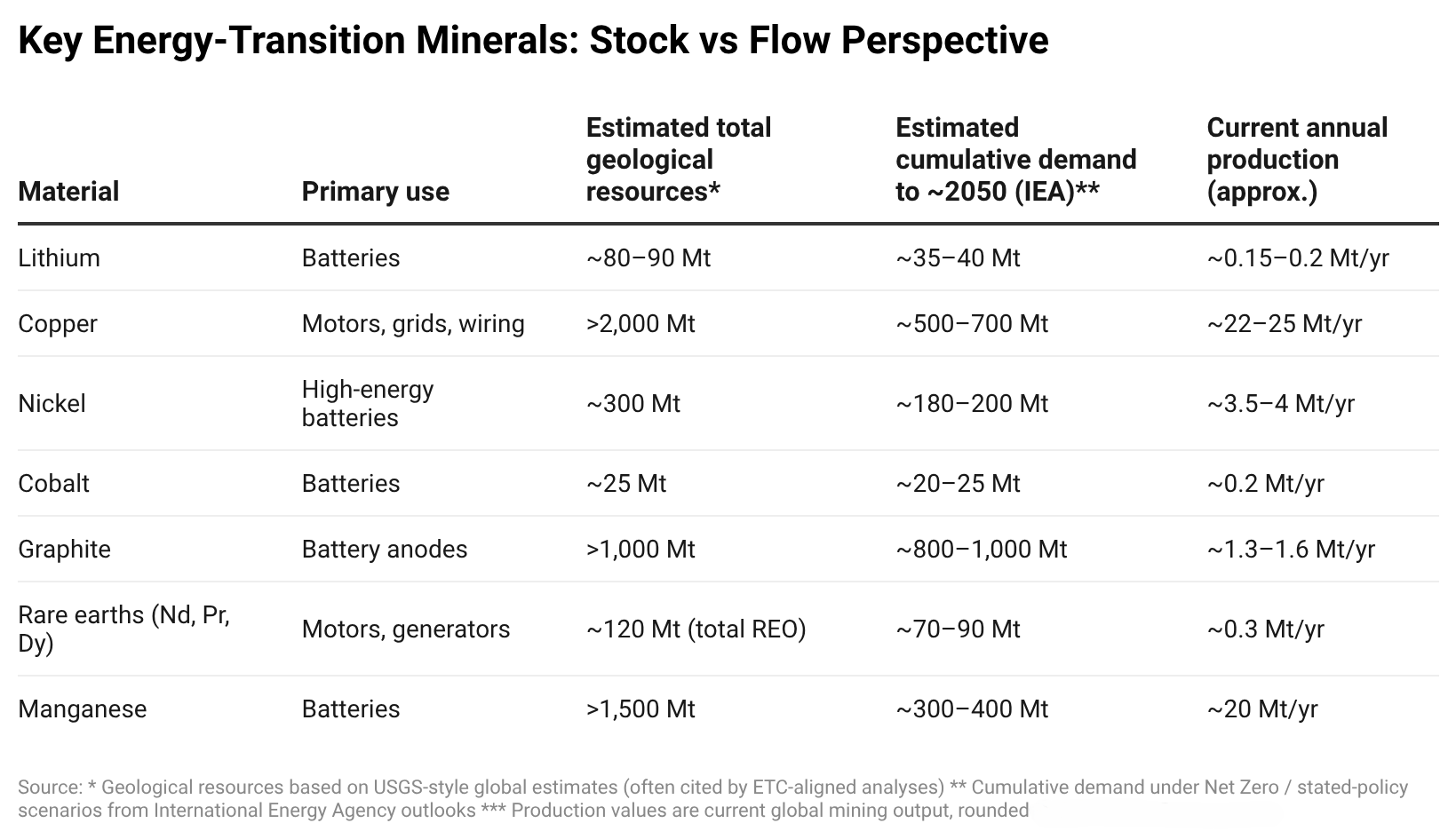

Geological availability vs transition demand

One source of confusion in this debate is that different organizations measure different things.

Groups often cited by ETC-style studies focus on total geological resources — what exists in the Earth’s crust, regardless of cost or timing.

The International Energy Agency (IEA) does something different: it estimates how much material would be required under specific energy-transition scenarios, such as Net Zero by 2050.

Placing these side by side is useful.

This comparison does not suggest long-term mineral scarcity, but highlights the scale and pace of production growth required over the next few decades.

What this table actually tells us

At first glance, this table supports Matt’s point:

for most materials, estimated transition demand through 2050 remains within known geological resources.

So this is not a “we will run out of minerals” argument.

The real issue is different.

Stock is not the same as flow

Geological availability answers one question:

Do the minerals exist?

Likely yes.

But the energy transition depends on another question:

Can we extract and process them fast enough, at scale, and at acceptable cost?

That is a flow problem, not a stock problem. As Matt notes, this does not imply long-term scarcity, but rather reflects short-term mismatches between supply growth and deployment speed.

Mining capacity, permitting timelines, refining bottlenecks, declining ore grades, and energy-intensive processing all limit how quickly supply can grow — even when resources are abundant.

This is why IEA reports often sound cautious despite acknowledging sufficient long-term resources.

Why this connects to battery technology

This also links directly to battery physics.

Today’s batteries have much lower energy density than fossil fuels. Lower energy density means:

more battery mass per vehicle

more copper in motors and wiring

more lithium, nickel, and graphite per unit of delivered energy

That increases material intensity, which in turn increases pressure on supply chains.

From this perspective, investment in higher-energy-density batteries, material efficiency, and recycling is not optional — it is structural.

Closing thought

So I largely agree with Matt: this is a technology transition.

But the technology challenge is not just batteries and renewables —

it is also our ability to scale material extraction and processing fast enough to match deployment goals.

Geology sets the ceiling.

Technology and supply chains determine whether we reach it in time.