Small data centers are paying five times too much for electricity

And the fix exists. The barrier is mostly regulatory, not technical.

Author’s note (April 29, 2026): Two corrections based on reader feedback.

First, smaller customers cannot access wholesale markets directly. What’s available in deregulated states are index-priced retail contracts from competing providers that track wholesale prices — not wholesale itself.

Second, ERCOT (Texas) is more accessible than PJM for smaller commercial customers. Texas has full retail deregulation with 100+ competing providers and no default utility option. PJM spans 13 states with inconsistent deregulation — switching rates in states like Pennsylvania sit around 35%, meaning most eligible customers never switch despite having the option.

The core argument stands. In regulated states like California, retail tariffs average $255/MWh with no legal alternative. In deregulated states like Texas, commercial customers average $91/MWh — still well above what active shoppers pay on index-priced contracts. The gap exists in both cases, for different reasons.

Large tech companies bypassed utilities entirely. Google, Microsoft, and Amazon sign long-term contracts directly with renewable energy generators — paying $30–55/MWh depending on region. Smaller data centers can’t. In most states, utilities hold the exclusive right to serve customers in their territory. Small and medium operators are locked into retail contracts paying $215–255/MWh — the same grid, four to six times the price.

This isn’t a secret. But the scale of the gap is worth looking at directly.

The price gap

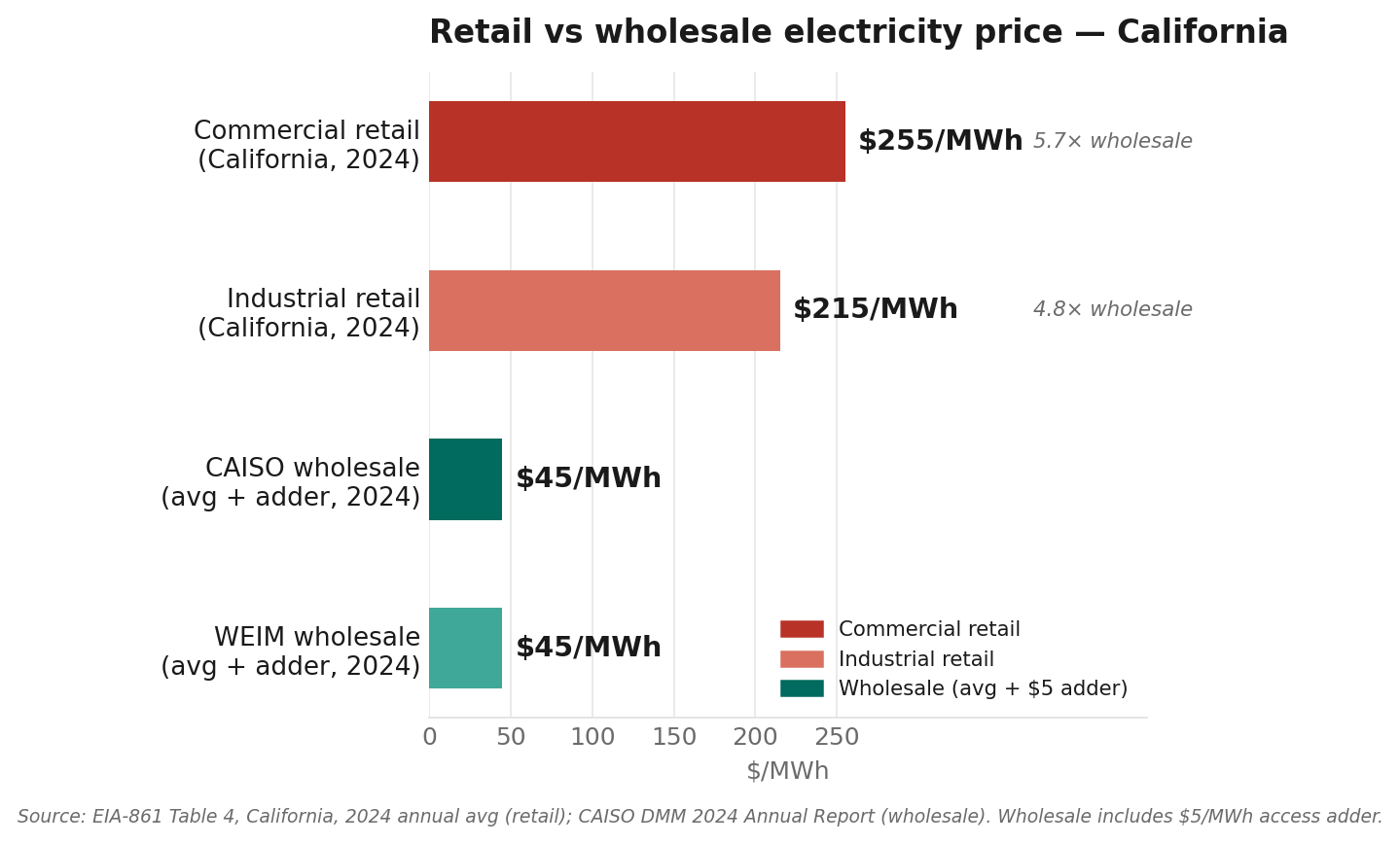

In California, commercial retail electricity averaged $255/MWh in 2024.¹ The CAISO/WEIM wholesale market averaged $40/MWh the same year.² Same grid, same electrons — different procurement path.

Industrial tariffs are lower — $215/MWh for California in 2024. Still nearly five times wholesale. Even after adding grid access and scheduling fees (roughly $5/MWh), the gap is large.

What this looks like in dollars

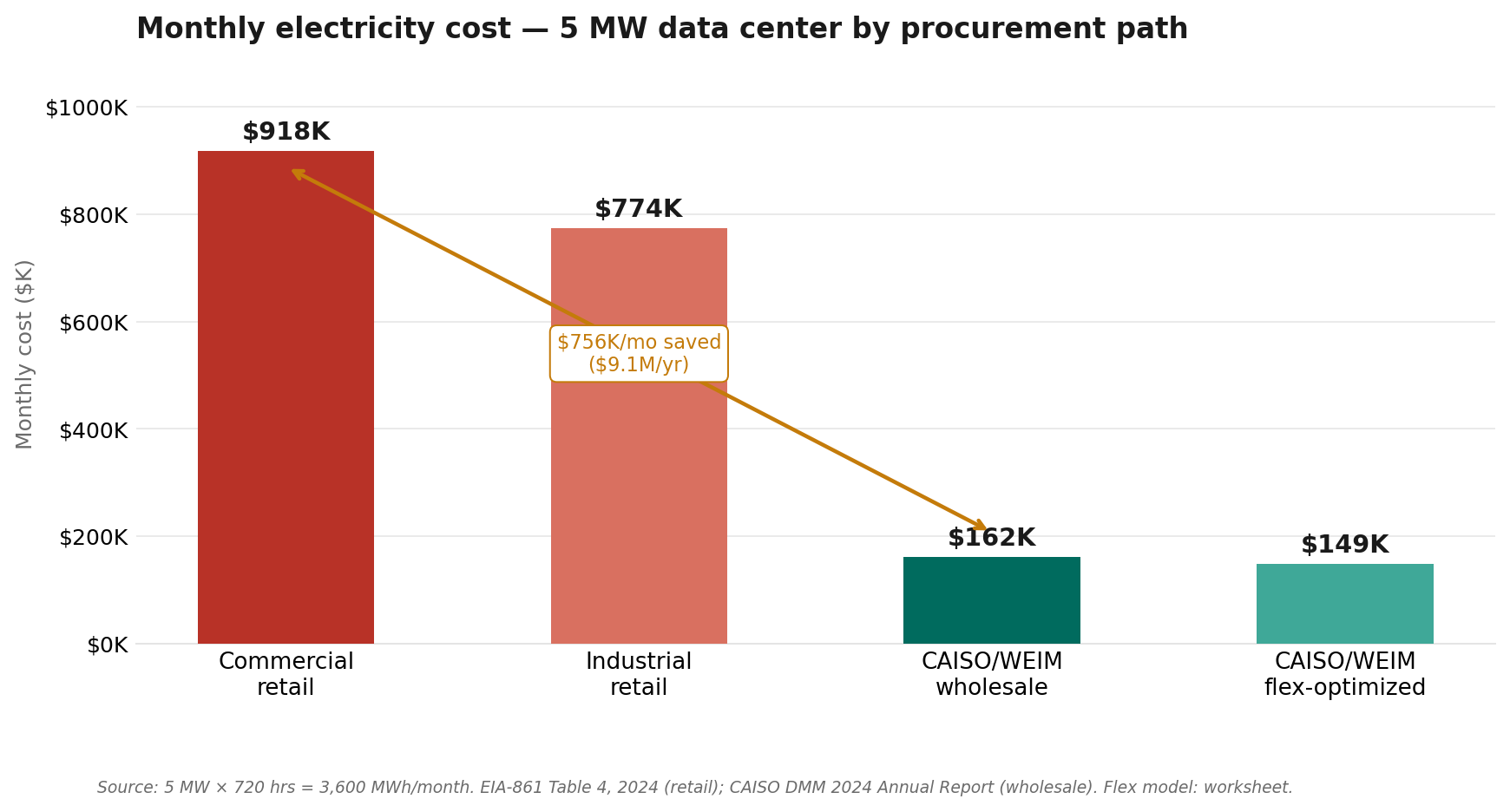

Take a medium data center — 5 MW average load, running 24/7. That’s 3,600 MWh per month.

A 5 MW data center on commercial retail pays $918K/month. The same load procured at wholesale pays $162K — a difference of $756K/month, or $9.1M per year.³

A small 1 MW facility leaves $151K/month on the table. These are not rounding errors. They are structural.

Why smaller operators are stuck

Two main reasons.

First, regulatory access. Most ISOs require entities to register as market participants to buy wholesale. This involves credit requirements and scheduling capability — not impossible, but not free or trivial.

Second, long-term utility contracts. Most small and medium data centers signed multi-year deals when they started. Breaking or renegotiating those is expensive. So they stay.

Large operators have the legal teams, credit ratings, and energy desks to navigate this. Small ones don’t — yet.

PJM is the clearest entry point

Not all markets are equally accessible. Among the major ISOs, PJM — covering the mid-Atlantic and Midwest — has the most relaxed participation requirements for demand-side customers. If you are a data center operator thinking about direct grid access, PJM is where to start.

This matters because the eastern US has high data center density. Northern Virginia alone accounts for 13–14% of global operational data center capacity — the largest single market in the world.⁴ The opportunity is concentrated exactly where the market is most accessible.

There is an additional upside: flexibility

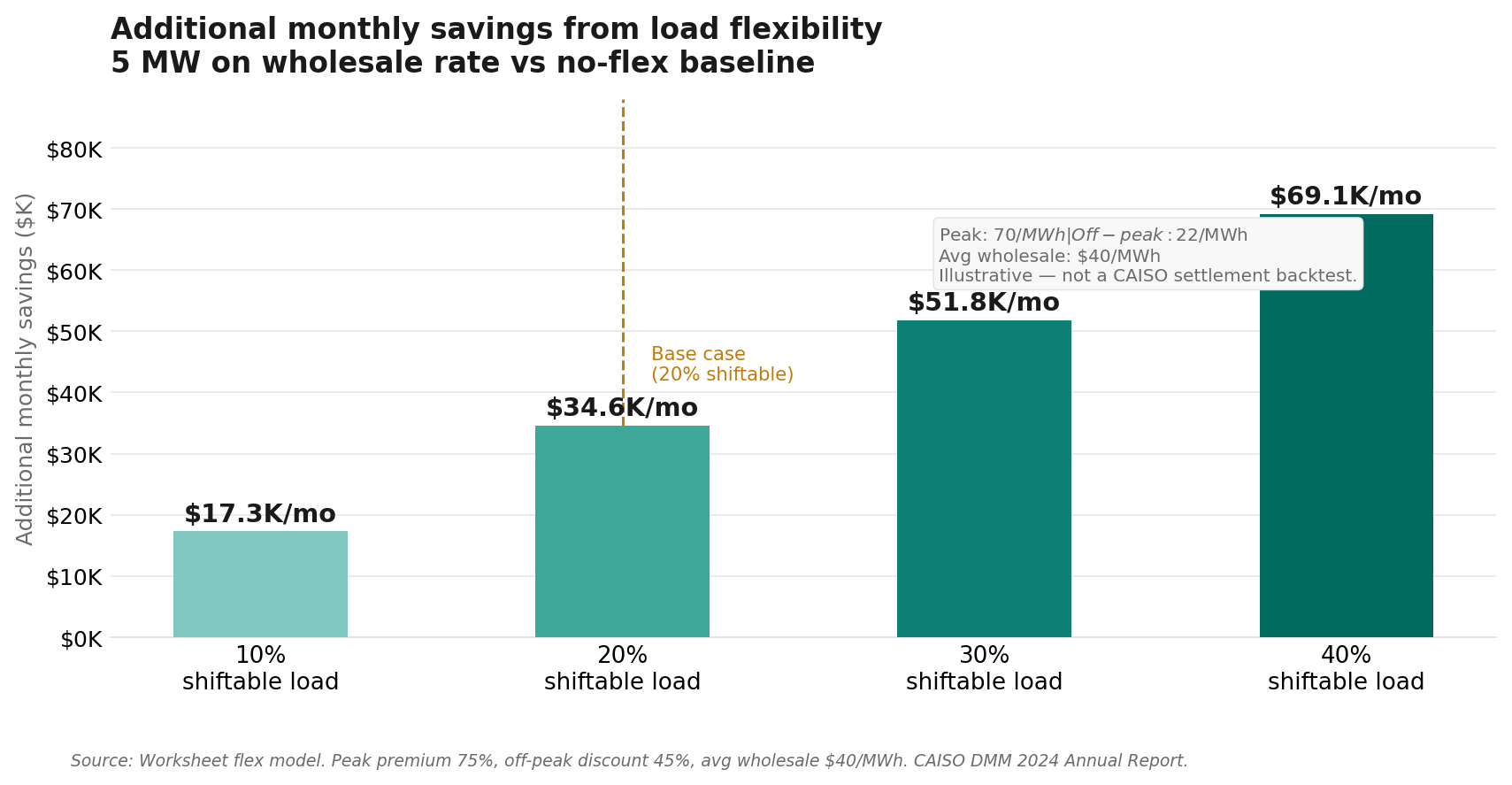

Getting on wholesale rates is step one. Step two is using flexibility to optimize within those rates.

Wholesale prices vary by hour. Workloads that can shift — AI training jobs, batch inference, model evaluation — can move from expensive peak windows ($70/MWh) to cheap off-peak ones ($22/MWh). Even shifting 20% of load saves an additional $34.6K/month on top of the procurement saving.

These numbers are illustrative — they depend on how much of a workload can actually move. But the direction is clear

The bigger picture

This connects to something I have been working on — a framework I call compute as virtual transmission. The core idea: flexible digital loads (data centers, EV charging, electrolysis) can absorb renewable energy that would otherwise be curtailed, by time-shifting consumption into windows of oversupply. That only works if these loads are connected to real-time price signals — not insulated from them by fixed utility contracts.

The tariff gap described here is one reason that coordination does not happen. Fixing procurement access is a precondition.

I published the full framework as a working paper earlier this year. It is on SSRN.

References

¹ EIA-861, Table 4: 2024 Total Electric Industry — Average Retail Price. California commercial: 25.54¢/kWh = $255/MWh; industrial: 21.53¢/kWh = $215/MWh. Released October 2025. https://www.eia.gov/electricity/sales_revenue_price/

² CAISO Department of Market Monitoring, 2024 Annual Report on Market Issues and Performance, August 2025. WEIM load-weighted average energy price, full year 2024. https://www.caiso.com/market-operations/market-monitoring/market-issues-and-performance-reports

³ Author’s calculation. 5 MW × 720 hrs/month = 3,600 MWh. Wholesale cost includes $5/MWh illustrative market access and scheduling adder.

⁴ Joint Legislative Audit and Review Commission (JLARC), Data Centers in Virginia, December 2024. https://jlarc.virginia.gov/landing-2024-data-centers-in-virginia.asp. Corroborated by Synergy Research Group (14%).