How the U.S. Can Strengthen Industrial Competitiveness in Heavy-Duty Electric Vehicles

The heavy-duty electric truck industry is going through a reset.

Global sales grew sharply from 2023 to 2024 (IEA Global EV Outlook 2025). But early data from BloombergNEF shows that 2025 sales have dropped significantly, especially in North America.

From what I see working in the heavy-duty EV world, the momentum we saw a year ago has slowed for U.S.

Across OEMs, fleet orders have gone down.

Some fleets paused purchases.

Some shifted back to diesel replacements.

This slowdown is an important signal.

It tells us something is misaligned in the U.S. strategy.

The message is simple:

heavy-duty BEV adoption is still fragile.

In this article, I want to share:

why adoption is slowing

what the U.S. is missing today

and how we can strengthen our industrial competitiveness in a practical way

The real bottleneck is price, not range

Many people think the biggest barrier for heavy-duty BEVs is range and lack of charging (fast) facilities.

But fleet owners tell a different story.

The real challenge is price.

Heavy-duty BEVs are expensive because:

large battery packs cost a lot

HV cables, converters, and inverters add cost

software and safety systems are new

R&D investments are high

production scale is still low

Fleets look at the total cost and ask a simple question:

“How do I justify replacing a diesel truck with something that costs more, takes longer to charge, and gives me less range?”

Until this changes, adoption will remain slow.

U.S. regulation is sending mixed signals

Under the Trump administration, the regulatory outlook for heavy-duty electrification is uncertain:

EPA’s Phase 3 GHG rules for 2027–2032 may be softened or delayed

Fleet-side rules like California’s ACF (Advanced Clean Fleets) have slowed down or become less predictable

There is more focus on domestic manufacturing and less on fleet incentives or ZEV adoption

In contrast:

Europe has strict long-term CO₂ reduction targets for HDVs (45% by 2030, 65% by 2035, 90% by 2040)

China offers direct subsidies, scrappage incentives, and operational benefits for new-energy trucks

The difference is simple:

Europe and China give fleets a stable path.

The U.S. does not.

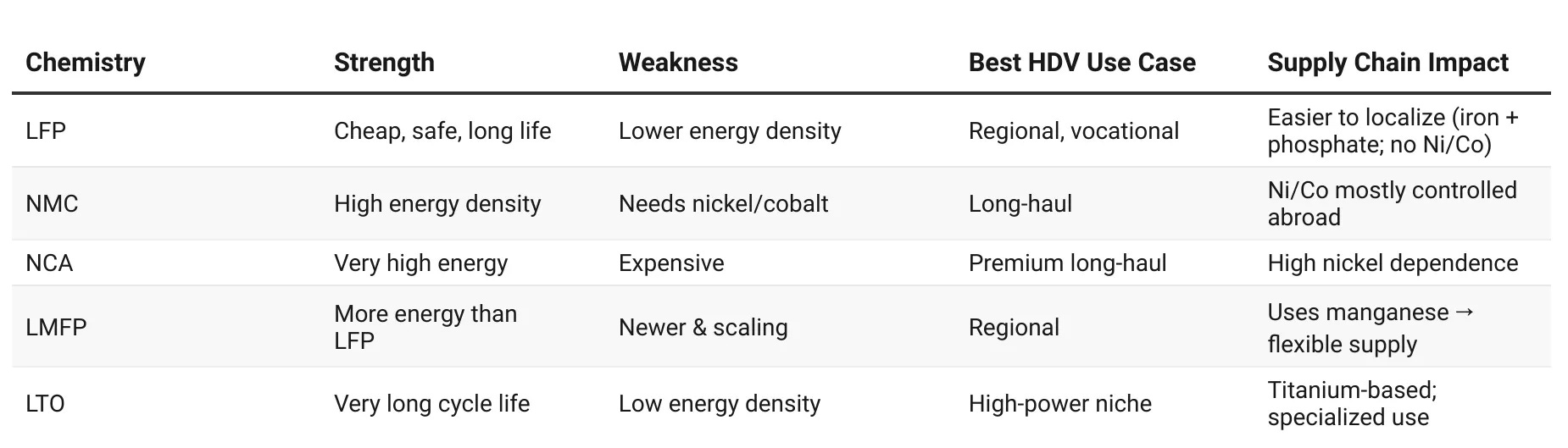

Heavy-duty EVs are not one category

One big misunderstanding in policy is treating all heavy-duty trucks as one group.

But the needs are very different as shown in the Battery technologies for

electric long-haul trucks:

A. Highway Long-Haul Trucks

Need high energy density

Need long range

Best served today by NMC or NCA batteries

B. Regional + Vocational Trucks

Shorter routes

Frequent stops

Can charge multiple times

Best served by LFP or LMFP

These differences matter because battery chemistry shapes the supply chain.

Logistics also must change — not just the truck

At ACT Expo this year, Volvo’s CTO said something important:

“We must redesign logistics, not just the vehicle.”

This is accurate. Today, freight is built around a diesel model:

one truck

one driver

long route

tight delivery window

But BEVs work best when the logistics system adjusts.

A. Hub-and-spoke routes

Freight moves through regional hubs; trucks run predictable shorter legs.

(Ref: NACFE Run on Less — Electric Depot)

B. Relay systems

One truck hands off a trailer to another at planned relay points.

(Ref: studies on freight relay networks)

C. Depot design

Multi-charger depot layouts allow fleets to scale from 5 BEVs to 50 BEVs (Ref: Electric Fleet Guide to EV Charging Overview).

D. Route optimization

Planning around charging windows, gradients, payload, and State of Charge (SoC).

In simple terms:

Instead of asking “Can one truck do the whole job?”

We should ask “How can the network share the job so BEVs fit naturally?”

A dual-track battery strategy is needed

To stay competitive right now, the U.S. should support the chemistries that work today:

Short-term (5–10 years)

NMC/NCA → long-haul

LFP/LMFP → regional & vocational

Localize precursor manufacturing

Reduce nickel/cobalt dependence

Incentivize domestic cathode & anode production

This protects current competitiveness.

But this only solves the short-term challenges.

To win long-term, the U.S. must invent the next battery

Here is the most important idea:

“The U.S. cannot beat China by copying China.

The U.S. can only win by inventing the next battery chemistry.”

China already dominates:

LFP

LMFP

NMC precursor supply

graphite anodes

large-scale cell manufacturing

Lithium-ion improvements today are small and incremental.

The U.S. should lead the next generation of batteries (Ref: Advancing energy storage: The future trajectory of lithium-ion battery technologies):

solid-state

lithium-sulfur

sodium-ion

zinc-based

Silicon-dominant anodes

metal-air

A breakthrough chemistry gives the U.S.:

new intellectual property

new manufacturing advantages

a new supply chain

cheaper vehicles for fleets

This is where America has natural strength: research and innovation.

A simple national strategy for heavy-duty electrification

To strengthen competitiveness, the U.S. needs a strategy that protects the present and builds the future.

Short-Term Strategy (Protect Today)

Pillar 1 — Dual-chemistry battery strategy

Use the best chemistry for each HDV segment.

Localize LFP, LMFP, NMC production as much as possible.

Pillar 2 — Balanced regulation for OEMs and fleets

OEM rules matter, but fleets make the purchases.

Fleet-side incentives must be stable and predictable.

Pillar 3 — Charging-Ready Freight Corridors

National Megawatt Charging System (MCS) corridors on major freight routes.

Streamlined permitting.

Battery-buffered depots.

Utility coordination.

Long-Term Strategy (Win the Future)

Pillar 4 — Invest in breakthrough battery chemistry

Lead the next battery — not the current one.

Build the future supply chain around American innovation.

These two tracks are not contradictory.

One protects the present. The other builds the future.

Final thoughts

Heavy-duty trucks move America.

Electrifying them is not simple — they pull >80,000 lbs and work in tough environments.

But the opportunity is huge.

The U.S. can lead again if we:

match chemistries to real use cases

support fleets, not just OEMs

rethink logistics so BEVs fit naturally

build charging corridors with certainty

invest boldly in new battery chemistry

America’s advantage is innovation — and that is how the U.S. can win the next decade of heavy-duty transportation.